Macro/Oil/Inflation/Geopolitics - Into The Void?

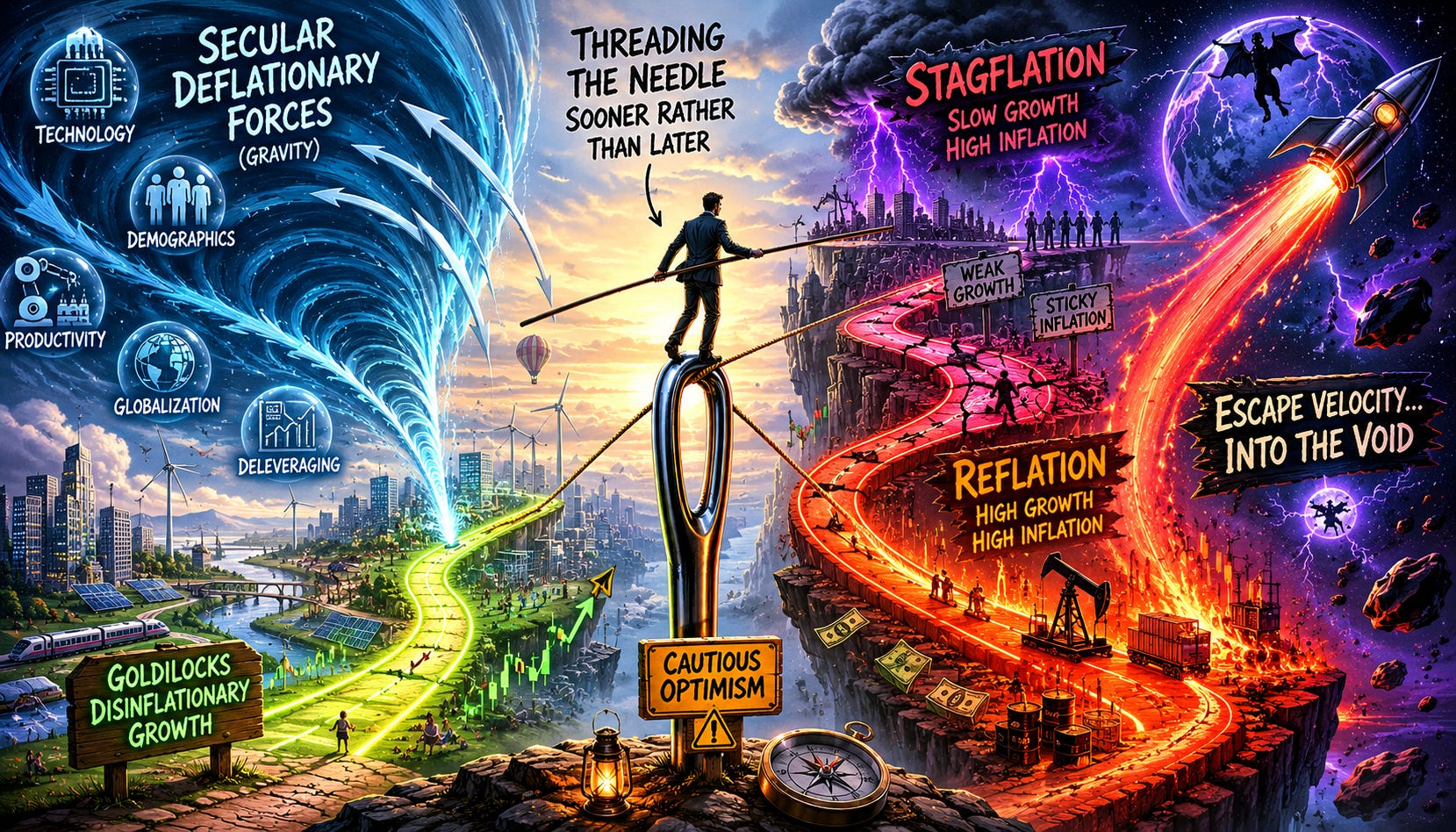

We are walking a tightrope between wildly divergent Macro outcomes, where one path leads to the Goldilocks of Disinflationary Growth, and another path leads into the void of Stagflation/Reflation.

We are walking a tightrope between wildly divergent Macro outcomes, where one path leads to the Goldilocks of Disinflationary Growth, and another path leads into the void of Stagflation/Reflation.

I was part of a roundtable at the LA branch of the SF Federal Reserve Bank last week, where I summarized some of these views. Each branch of the Fed conducts …