Weekly KAOS, 6/5/26

Hormuz, Hegseth, and the Gold Crossover (or not)

Welcome to the Weekly KAOS — UrbanKaoboy’s end-of-week roundup covering Macro and Geopolitics, where I try and tease out the most impactful bits of the week.

Themes of the Week

Three months into the Iran war, Hormuz is still the Macro linchpin while Gold quietly dethrones Treasuries on central-bank balance sheets (or not)

Three months into the Iran war and we still don’t have a deal. To borrow from Michael Every, the pattern is Zeno’s dichotomy dressed up as diplomacy — both sides agree on the broad shape of a 60-day ceasefire extension, a Hormuz reopening, a sanctions-for-constraints swap — and then keep halving the distance over sequencing and signatures.

I have another mythological mental model: The Tantalus Tease

Meanwhile the IRGC keeps lobbing drones at Kuwait’s airport, we keep hitting Qeshm, and BBC Verify’s satellite analysis now counts twenty US military sites damaged since the shooting started. This is the Han Solo asteroid-field run I laid out in last week’s Weekly KAOS — except Han hasn’t found the hole yet, and the chokepoint that was supposed to be a bargaining chip has become the IRGC’s principal leverage.

The week’s KAOS confirms the structural call: Oil is the Macro linchpin, Inflation is seeping back in via a side door nobody is watching (Chinese refined-product exports — Beijing refining only for domestic demand, exporting zero product, lifting global product prices straight into Western core), and the Mag7 tape is pushing into a 10-week run matched only by Dec ‘99, Aug ‘20, and Jun ‘24 — all three followed by drawdowns inside 40 trading days. Watch for my interview tomorrow about this.

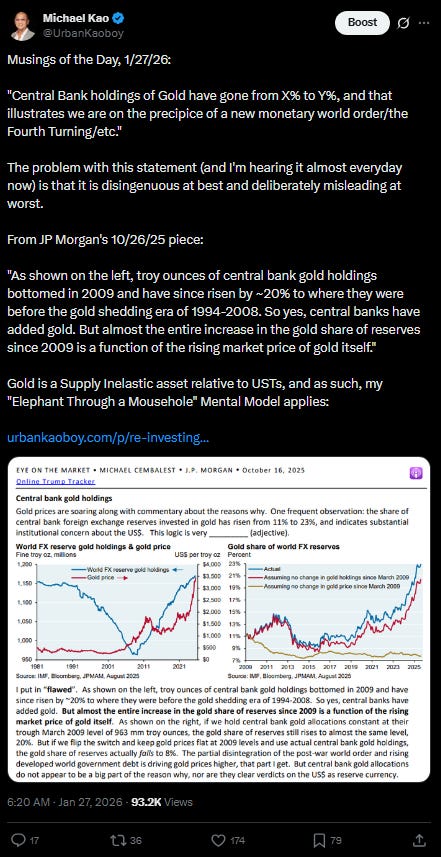

In other news, the ECB made a big point in showing how Gold has overtaken US Treasuries as the world’s top reserve asset, 27% versus 22%, with total USD-denominated reserves down to 42% from roughly 60% twenty-five years ago.

Too bad they forgot to tell you that it was mainly because of the price movement of Gold:

The Sword of Inelastic Supply cuts both ways, and this week’s carnage in Gold prices reminds you why it won’t supplant the UST as the primary central bank reserve asset.

My standing view is that USD/UST hegemony rests on geographic balance-sheet assets — waterways, arable land, blue-water navy — that no rival can match, and I still think that’s right at the level of National Power.