Re: Oil-GS Call for $90 Brent by YE’21.

GS out with a chart pack today, calling for “next leg higher in oil prices - from a cyclical to a structural bull market.” Summary points/editorial to follow.

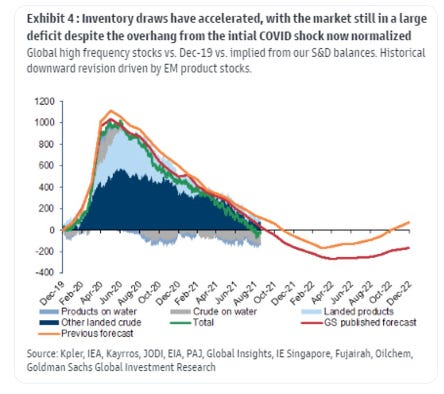

“This dynamic has led to a historic 4.5 mb/d deficit, which should lead inventories to fall to their lowest level since 2013 by year-end...”

Two charts tell the story. Here’s supply:

Here’s demand: